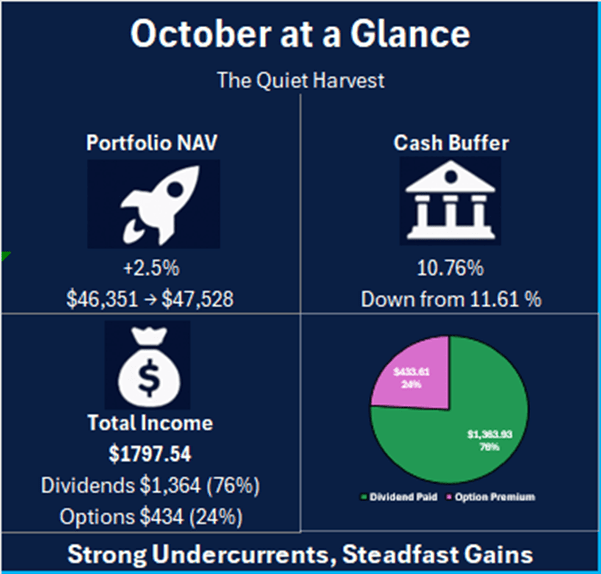

Slow Hands, Steady Gains

Growth +2.5%

Dividends $1,363.93

Option Income $433.61

Cash Reserve 10.76%

🖋️ Foreword

October unfolded as a quiet yet defining month for both the market and my portfolio. Beneath the calm surface, undercurrents surged, as the cycle began to take shape anew.

Technology once again led the charge. OpenAI deepened its strategic partnerships with NVDIA, AMD and Broadcom, securing access to cutting-edge GPUs while co-developing custom AI accelerators that close the gap between model design and silicon performance. The newly launched Stargate initiative, a multi-billion dollar joint venture with SoftBank Group, set in motion the construction of next generation AI data center campuses around the world. At the enterprise level, OpenAI expanded its reach through collaborations with Databricks, integrating its frontier models across more than 20,000 corporate data platforms, and with Guardian Media Group, gained licensed content for both training and real-time use within ChatGPT. Together, these moves have established OpenAI’s presence across the entire AI stack, reigniting strength in the semiconductor and enterprise AI sectors while lifting broader market sentiments.

For YieldMax investors, such as myself, a quieter but equally important transformation took place. MSTY and CONY completed their transition to weekly dividends, joining ULTY in providing a steadier and more predictable stream of income. The timing of this shift was no coincidence. As crypto markets settled into tighter trading ranges and volatility declined, option premiums linked to MicroStrategy and Coinbase began decaying faster than before. By syncing payouts with their weekly option cycles, YieldMax ensured a more consistent flow of yield even as the broader crypto sector remained muted.

The macro environment, however, was far from calm. Gold surged past $4,350 mid-month before easing to $4,002.81 by the close, still up 3.6% for October. The move reflected a flight to safety as the U.S. government shutdown dragged on, with negotiations over fiscal spending and federal funding still unresolved. Markets began to price in the growing risk of delayed data releases and reduced policy clarity, pushing investors toward defensive assets and income-based strategies. Overseas, focus turned to Seoul, where President Trump met President Xi Jinping in an attempt to recalibrate trade and security relations. The dialogue was constructive but cautious, producing reassurances without concrete agreements. The meeting underscored a geopolitical backdrop defined by pragmatism rather than partnership.

In the United States, the Federal Reserve cut interest rates by 25 basis points but warned that no further reductions were likely this year. The move signaled confidence that inflation was cooling within expectations, though the ongoing government shutdown complicated the near-term outlook. Liquidity held steady, yet investor caution grew as federal data gaps limited visibility. With the shutdown still unresolved and diplomacy treading cautiously abroad, October proved to be a test of patience and conviction across markets.

In the cryptocurrency space, Bitcoin retreated 3.9%, falling from highs near $125,000 to around $109,000, while Ethereum held steady near $3,400. Trading volumes thinned through the latter half of the month, signaling a shift toward accumulation rather than capitulation. For crypto-linked assets such as MSTY and CONY, this quieter environment provided the ideal backdrop for their transition to a weekly dividend model, mirroring the structure that had already proven successful with ULTY.

Through all these currents, the portfolio remained composed. NAV rose 2.5% to $47,528, supported by weekly dividends, disciplined option income, and a strong cash reserve. October may have been marred by uncertainty, but at the portfolio level, it stood calm and quietly resilient.

Let’s unpack it.

🖼️ Visual Summary

🔑Key Takeaways

- NAV Rose Steadily

The portfolio’s value increased by 2.5% in October, closing at $47,528. Total Equity grew by $1,177, a modest but steady gain even though the market faced tricky and cautious conditions. Growth was supported by consistent yield and offsetting the effects of policy uncertainty and the ongoing government shutdown. - Income Flow Remained Firm

Total income reached $1,797 (+24.9%), comprising $1,364 (+10.4%) in dividends and $434 (+112.6%) from option premiums. The transition of MSTY and CONY to weekly dividends is now complete. With this change, the entirety of the Yield Engine now pays weekly, providing a stable flow of cash. - Liquidity Reserve Slightly Reduced

The Liquidity Reserve closed at $5,113 (10.8% of NAV), down slightly from September (-1.8%). The small reduction reflected controlled reinvestment into income-producing positions while maintaining enough flexibility for tactical opportunities in November. - Yield Engine Consolidated

The Yield Engine closed $22,044 (-12.6%), as MSTY and CONY adjusted to their new weekly payout model. These paper declines were largely offset by $1,364 in realized dividend income, illustrating the trade-off between capital stability and ongoing yield. The segment continues to deliver predictable cashflow, maintaining its purpose as the portfolio’s core income driver. - ETFs Led the Recovery

ETF holdings (CSPX, IWDA, VWRA) rose from $6,725 to $7,342 (+9.2%). Broader market resilience and defensive rotation supported global equity ETFs, which continued to serve as the portfolio’s stabilizing anchor amid yield-segment volatility. The category remained a reliable contributor to NAV growth, reinforcing the long-term base of the portfolio. - Tactical Yield Expanded

SOFI rose from $3,963 to $7,420 (+87.2%), driven by accumulated options income and tactical position scaling. The increase reflected a blend of capital appreciation and consistent premium harvesting from short-term put and call strategies. The position continued to serve as a flexible yield engine within the portfolio, complementing the steady weekly income produced by the YieldMax suite. - Tech & Growth Strengthened

Tech and growth stocks rose 9.0%, led by NET (+18%), NVDA (+8.5%), and PLTR (+9.9%). The sector benefited from renewed optimism following OpenAI’s expanded partnerships with major chipmakers and data firms, strengthening the long-term AI narrative. - Exploratory Growth Advanced

Exploratory holdings increased $1,455 (+15.3%), supported by gains in 640 (+12.4%) and 9MT (+18.2%). Although still small at 3.1% of NAV, this segment adds regional and sector diversity, with selective exposure to emerging opportunities. The move in 640 also reflected its recent share consolidation, a structural change rather than a price catalyst. - Portfolio Structure Reinforced

The framework continues to work well, offering clarity, balance, and direction for capital deployment. Each segment contributed to stability in a month defined by shifting global conditions, disciplined reinvestment, and consistent income generation.

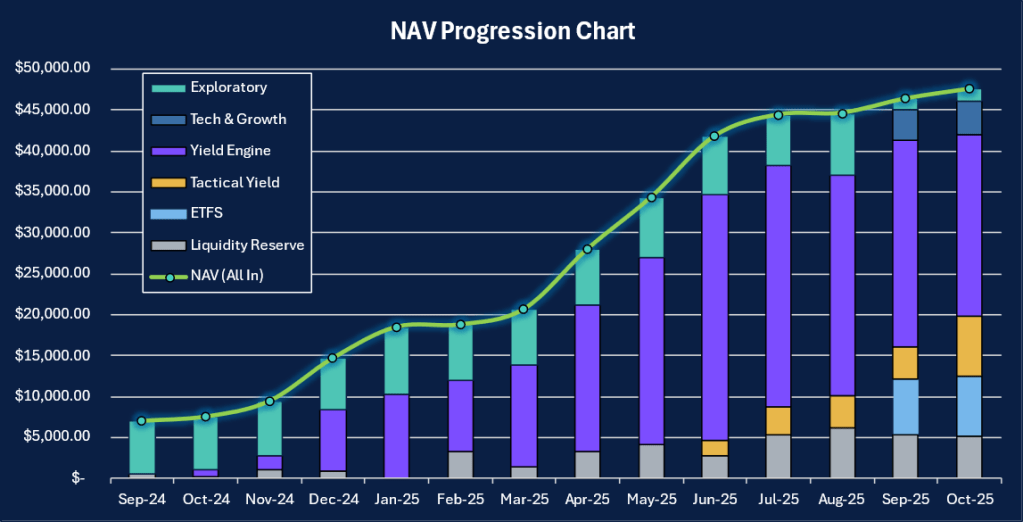

📊 NAV Progression

October closed with the portfolio at $47,528, up 2.5% from September’s $46,351. The increase was modest but steady, marking the fourth straight month of growth even as markets moved cautiously through rate cuts, fiscal uncertainty, and the ongoing government shutdown.

Performance this month was led by Tactical Yield, where SOFI nearly doubled to $7,420. Accumulated option income and controlled scaling helped it capture volatility that other segments avoided, turning short-term market hesitation into yield.

The Yield Engine softened to $22,044 (–12.6%) after MSTY and CONY adjusted to their new weekly payout rhythm. Yet, the segment’s consistent distributions continued to anchor overall income, cushioning the drawdown with $1,364 in realized dividends.

ETFs provided quiet strength, rising 9.2% to $7,342. They offered balance through defensive exposure to CSPX, IWDA, and VWRA, which absorbed volatility from income assets.

Meanwhile, Tech & Growth added momentum, up 9.0% to $4,152, as optimism around OpenAI’s expanding AI partnerships reignited sentiment across semiconductor and enterprise technology names.

The Exploratory Growth segment grew 15.3% to $1,455, helped by 640 and 9MT, with the latter’s regional exposure adding quiet strength. 640’s recent share consolidation adjusted its trading profile without changing underlying value, keeping this category’s contribution measured yet meaningful.

Finally, the Liquidity Reserve settled at $5,113 (10.8% of NAV), maintaining flexibility for new opportunities in November while sustaining a comfortable buffer.

Together, these movements painted a month of controlled progression. Tactical execution at the edges, quiet consistency at the core, and a portfolio structure that continues to function exactly as designed.

🧩Portfolio Updates

ETFs Expanded

2 IWDA shares and 1 VWRA share were added in October, modestly increasing total ETF exposure. The ETF layer now stands at $7,342 (+9.2%). This expansion strengthened the base of long-term compounding while providing balance against higher-yield segments. Global indices remained stable despite macro uncertainty, and these selective additions ensured continued participation in the broader equity recovery.

Yield Engine Reinforced

An addition of 200 ULTY shares brought total holdings to 1,500, reinforcing the weekly dividend foundation. MSTY and CONY maintained their share counts but officially completed the transition to weekly payouts, aligning with ULTY’s schedule. Although MSTY fell 22.0% and CONY declined 7.8%, the segment still generated $1,364 in dividend income. This steady flow preserved momentum and reaffirmed the Yield Engine’s role as the portfolio’s income anchor.

Tactical Yield Grew

The SOFI position increased from 150 to 250 shares, supported by deliberate scaling and active option management. Its value rose 87.2%, reflecting both capital appreciation and consistent premium collection. Option income totaled $434, confirming SOFI as the portfolio’s most flexible and responsive source of yield heading into the final quarter of the year.

Tech & Growth Retained

No new positions were added within Tech & Growth, but existing holdings performed well. NET gained 18%, NVDA rose 8.5%, and PLTR advanced 9.9% as enthusiasm returned to the AI and semiconductor sectors following OpenAI’s expanded industry partnerships. The segment continues to provide targeted exposure to innovation while remaining proportionally small to preserve overall portfolio balance.

Exploratory Footprint Initiated

No share changes occurred within the Exploratory sleeve, yet total value rose 15.3% to $1,455. Gains in 640 and 9MT, along with 640’s share consolidation, improved trading stability and visibility. Though small at 3.1% of NAV, this sleeve adds regional and small-cap diversification that supports long-term growth potential.

Liquidity Managed

Cash reserves closed at $5,113, representing 10.8% of NAV, slightly lower than September’s 11.6%. The reduction came from reinvestments into ETFs, ULTY, and SOFI, reflecting measured capital deployment rather than reduced liquidity discipline. The reserve remains healthy and ready for tactical opportunities in November.

🌐 Market Update

Volatility & Rates

What was expected

Investors entered October expecting a calm environment. The market consensus was that the Federal Reserve’s 25-basis-point rate cut would provide short-term support to equities and ease funding costs without reigniting inflation. Many believed the government shutdown would be resolved quickly, minimizing impact on liquidity or data flow. Volatility was expected to stay contained, with attention shifting back to corporate earnings and macro normalization.

What happened

The Fed followed through with the rate cut, but its tone turned unexpectedly firm. Policymakers signaled that no further reductions were likely this year, dampening expectations for a prolonged easing cycle. Meanwhile, the shutdown dragged on, leaving investors without official data on employment, CPI, and growth. The absence of reliable indicators increased market hesitation.

Gold climbed to $4,350 mid-month before settling at $4,002.81, closing 3.6% higher. The rally reflected demand for safety as confidence in fiscal management weakened. Treasury yields held stable, and equity volatility remained moderate, but risk appetite narrowed sharply toward defensive positioning.

How the portfolio responded

The portfolio leaned on its internal rhythm of consistency. Weekly distributions from the Yield Engine maintained cashflow even as prices softened. The ETF layer provided additional stability, rising 9.2% as global markets steadied. Liquidity remained intact at 10.8%, preserving tactical flexibility. Rather than chase market relief, the portfolio held course, focusing on cash generation and steady reinvestment.

Crypto & Equity Performance

What was expected

Coming into the month, the crypto market was projected to consolidate after September’s rally. Analysts anticipated tighter trading ranges, with Bitcoin hovering near $120,000 and Ethereum around $3,400. The expectation was for lower volatility and sustained premiums for option-based yield strategies. On the equity side, investors looked for continued momentum in technology, supported by optimism around AI adoption and stable earnings.

What happened

Bitcoin declined 3.9%, sliding from near $125,000 to around $109,000, while Ethereum held steady near $3,400. Trading volumes thinned as speculative interest waned. Option premiums decayed faster than expected, prompting MSTY and CONY to transition to weekly dividends to align payouts with realized income.

Equity markets remained resilient. OpenAI’s expanded partnerships with NVIDIA, AMD, and Broadcom boosted semiconductor optimism, while the Stargate initiative with SoftBank Group reinforced confidence in large-scale AI infrastructure. Collaborations with Databricks and Guardian Media Group extended OpenAI’s enterprise reach, driving renewed interest across AI-linked equities. NET (+18%), NVDA (+8.5%), and PLTR (+9.9%) all advanced, while broader indices traded sideways amid caution.

How the portfolio responded

The portfolio’s income design absorbed the crypto slowdown smoothly. The Yield Engine continued generating steady payouts, offsetting short-term valuation dips in MSTY and CONY. The Tactical Yield sleeve, led by SOFI, captured market inefficiencies through short-dated put and call strategies, producing an 87.2% gain for the month. ETFs added quiet balance, rising 9.2% and reinforcing the defensive core. Overall, the portfolio finished 2.5% higher, driven by disciplined management rather than market momentum.

Outlook for November

November begins with a mix of caution and opportunity. The government shutdown continues, leaving markets data-blind but not directionless. Rate policy has stabilized, and inflation pressures appear contained, suggesting a potential window for tactical yield strategies.

For the portfolio, the focus remains unchanged. The Yield Engine’s synchronized weekly cycle will sustain predictable income. SOFI’s Tactical Yield positioning will continue to exploit short-term volatility selectively, while ETFs anchor long-term stability.

Patience will again be the priority. With rates steady, income reliable, and liquidity preserved, November is expected to reward disciplined accumulation rather than aggressive rotation.

🎯Objective Review

Here’s how we performed against our August targets at a glance:

Base Goals

✅ Income Goal: Generate at least $1,300 — Exceeded

Total income reached $1,797, comprising $1,364 in dividends and $434 in options premiums. The transition of MSTY and CONY to weekly payouts strengthened the portfolio’s income rhythm, providing smoother and more consistent cashflow than in prior months.

✅️ Cash Reserve: Maintain between 10% and 12% of NAV— Met

Reserves closed at $5,113, or 10.8% of NAV, slightly below September but still within the target range. The small drawdown reflected controlled redeployment into ULTY and ETFs while maintaining adequate flexibility for tactical entries in November.

✅ Option Selling: Focus only if premium exceeds 2.5% — Met

SOFI remained the sole active option engine for October, involving four key trades across both puts and calls.

- Average realized yield: 3.2% per trade (above the 2.5% benchmark)

- Highest yield: 4.5% on the 26.5 Put (Oct 31 expiry)

- Assignment: 1 Put at $27, establishing 100 shares at an effective cost of $26.52

- Net premium earned (after all Buy-to-Close and fees): $434

✅ Yield Engine Stability: Hold through volatility — Met

Despite short-term drawdowns in MSTY and CONY, distributions remained uninterrupted. ULTY rose 4.6% following capital additions, reinforcing total portfolio yield stability even as prices fluctuated.

Stretch Goals

✅ Total Income: Exceed $1,500 — Achieved

Monthly income totaled $1,797, well above the stretch target, supported by synchronized weekly payouts and active SOFI premiums.

✅ NAV Growth: Add $2,000 to $3,000 — Partially Met

Portfolio NAV grew 2.5%, from $46,351 to $47,528, a gain of $1,177. The slowdown was largely due to MSTY price compression, though steady income offset most of the capital drag.

✅ Strategic Deployment: Add to CSPX, IWDA, or ULTY selectively — Met

Additional 200 ULTY shares were acquired, alongside ETF reinforcements in CSPX and IWDA. These additions strengthened both yield and stability layers ahead of the November cycle.

✅ Risk Discipline: Maintain controlled exposure — Met

Only one SOFI option was open at any given time, and all short legs were closed or rolled before expiry. This preserved capital safety and kept exposure aligned with volatility shifts.

✅ Exploratory Layer: Maintain below 3% of NAV — Met

640 and 9MT advanced modestly (+12% and +18% respectively) while staying within allocation limits. This layer continued to provide small but meaningful diversification benefits.

📁Transactions

October Transactions

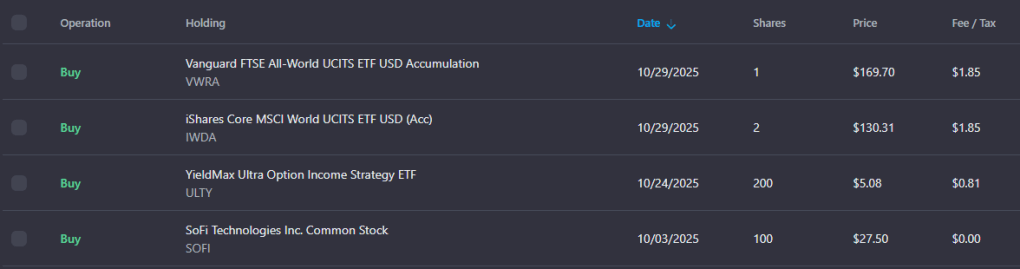

- ULTY

Purchased 200 shares at $5.08 on October 24, expanding the core Yield Engine allocation to 1,500 shares in total. This addition reinforces the portfolio’s weekly income base and improves yield consistency going into November. - IWDA

Added 2 shares at $130.31 on October 29, strengthening global developed market exposure. The move complements CSPX and aligns with the objective of gradual reinforcement of the ETF layer for long-term stability. - VWRA

Purchased 1 share at $169.70 on October 29. This incremental addition broadens passive exposure across both developed and emerging markets, rounding out the Global Core ETF segment. - SOFI

Acquired 100 shares at $27.50 on October 3 after put assignment. The new shares formed part of the tactical yield sleeve and enabled covered call positions later in the month, maintaining continuous premium generation within controlled risk limits. - Liquidity Reserve

The cash balance adjusted downward following reinvestments into ULTY and ETFs. The portfolio closed with a reserve of $5,113, equal to 10.8% of NAV, preserving sufficient flexibility for tactical opportunities in November.

🏦 Income Overview

October delivered $1,797.54 in total income, a 24.9% increase from September. Dividends made up $1,363.93 (76%), while options contributed $433.61 (24%). The income mix continued to lean toward stable, recurring distributions while retaining tactical upside from options.

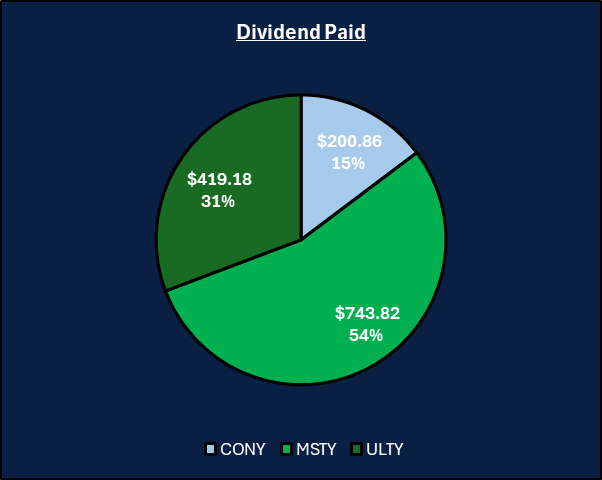

Dividend Highlights ($1,364)

- MSTY: $743.82, a slight increase compared to September.

- ULTY: $419.18, distributions increased due to additional ULTY additions

- CONY: $200.86, a slight increase compared to September.

Option Activity ($434)

- All option trades in October came from SoFI

- 4 short puts were opened and closed profitably, with one position assigned at the $27 strike, creating 100 new shares at an effective cost basis of $26.52 after premiums.

- 1 short call was sold at the $32 strike and later bought back for a small gain, maintaining position flexibility as SOFI consolidated near $28–29.

- Average yield on strike: 3.2%, with the highest single trade return at 4.5% on the $26.5 put (Oct 31 expiry).

- Average holding period: 7–10 days, keeping exposure short and responsive to price movement.

Yield Profile

- Overall Yield: 3.2 %

- Dividends: 3.2 %

- Options: 1.0 %

Another month of stable performance across all yield engines. The portfolio’s blended yield of 3.2% demonstrates the balancing of passive income strength with active yield enhancement.

🔭 Next Steps

November will focus on maintaining rhythm rather than expansion. With all YieldMax funds now paying weekly, the income engine is fully synchronized. The plan is to preserve this, manage SOFI options selectively for tactical yield, and gradually strengthen ETF positions on meaningful pullbacks. Cash reserves will remain above 10% to safeguard flexibility while monitoring opportunities as volatility and policy signals unfold.

Area of Focus

- Maintain income Discipline

With all YieldMax funds now aligned to weekly payouts, the focus shifts toward maintaining consistency rather than expansion. The goal for November is to sustain income above $1,700, keeping weekly flows uninterrupted while monitoring MSTY and CONY for any payout drift following their transition. - Tactical Option Rotation

Continue managing SOFI through short-duration puts and selective covered calls, targeting 2.5% or higher returns on strike. Maintain only one active position at a time to preserve risk control and liquidity. If volatility expands post-shutdown resolution, consider widening strikes slightly for improved premium capture. - Reinforce ETF Stability

Gradually increase CSPX and IWDA on meaningful dips to strengthen the defensive layer. ETF adds remain the foundation of long-term compounding and will serve as the stabilizer should volatility return in late Q4. - Preserve Liquidity Buffer

Keep the cash buffer above 10% of NAV. With volatility lingering and rate direction uncertain, the reserve will remain essential for opportunistic entries and capital protection. Avoid large deployments until macro clarity improves. - Monitor Yield Sustainability

Track the effective yields of MSTY and ULTY relative to NAV. If price pressure continues without distribution erosion, consider selective reinvestment to compound weekly returns at more attractive valuations.

📅 Month 14 Objectives

✅ Base Target

- Income Goal:

Generate at least $1,700 in total income, primarily through weekly dividends from MSTY, CONY, and ULTY, supplemented by tactical SOFI options. Maintain continuity in distributions and protect the month’s payout rhythm. - Liquidity Reserve:

Keep reserves between 10% and 12% of NAV to preserve flexibility for tactical entries. Avoid new large-scale deployments until market clarity improves following the ongoing shutdown and Fed policy recalibration. - Equity Exposure:

Add selectively to CSPX or IWDA on meaningful pullbacks. Focus on strengthening the ETF base to balance yield-driven segments and reduce sensitivity to market volatility. - Option Selling:

Continue using SOFI short puts and covered calls only if returns exceed 2.5% of strike value with expiries under 14 days. Maintain single-position exposure at all times to control leverage and margin usage. - Yield Engine Stability:

Hold MSTY, ULTY, and CONY through short-term volatility. Reinvest only if prices decline more than 5% without a reduction in distribution. The priority remains yield sustainability, not price recovery.

🚀 Stretch Goal

- Total Income:

Exceed $1,900 through combined weekly dividends and optimized option premiums. - NAV Growth:

Increase NAV by $1,500 to $2,000, driven by earned income and incremental ETF reinforcement. - Strategic Deployment:

Allocate up to $1,000 into ETFs if market weakness deepens mid-month, reinforcing the stability pillar before year-end distributions. - Risk Management:

Maintain portfolio delta near current neutral levels. Avoid overexposure to crypto-linked volatility until BTC sustains above $115,000 for two consecutive weeks. - Exploratory Layer

Monitor 640 (HKEX) and 9MT (SGX) for volume-based breakouts. Add only upon confirmation of strength and keep allocation under 3% of NAV.

The goal is to let structure do the work. To stay patient, keep yield steady, and let the compounding take care of the rest.

🧠 Final Thoughts

October was a month of quiet strength. The market shifted beneath the surface, yet the portfolio held its rhythm. Weekly income flowed as designed, the Yield Engine ran smoothly, and tactical discipline around SOFI kept risk contained while adding meaningful yield.

The shift of MSTY and CONY to weekly dividends marked a structural milestone, turning the portfolio into a true weekly income system. Each segment functioned in balance, showing that consistency can sometimes outperform excitement.

As November begins, the focus remains on maintaining tempo rather than expansion. The target is to preserve steady cashflow, keep reserves above 10%, and reinforce the ETF base on meaningful dips. The aim is not to chase volatility but to let structure and rhythm do the work.

Strong undercurrents remain, but the gains remains steadfast.

💬 Let’s Talk

October reminded me that discipline is often the quietest strength in investing. The past month was not driven by headlines or surprises but by steady income, measured positioning, and patience rewarded in small, consistent increments.

What are you focusing on this quarter? Are you building yield, reinforcing your base, or waiting for volatility to return before redeploying?

Share your thoughts below.

Leave a comment